Looking Through Institutional Portfolios

Institutional positioning, tech dominance, and why breadth matters

Today is the deadline for investment managers with more than $100 million in assets under management to file their quarterly holdings report (Form 13F) with the SEC, which means, for me, a day to look over what some of the most well-known fund managers in the world have been doing with their money (and, in many cases, their clients’ money).

These filings offer a delayed but still valuable snapshot of how major hedge funds and institutional investors positioned themselves at the end of the last quarter. While they don’t show everything, such as short positions, private investments, or many derivative strategies, they can still reveal meaningful shifts in conviction, new positions, and changes in exposure to certain sectors or themes.

This is why proper due diligence is so important. None of us has insight into the full context behind why a fund is holding certain positions or how those positions fit into a broader strategy.

For example, a portfolio might show a long position in a company like Cameco, which could easily be interpreted as a bullish view on uranium. However, that interpretation could be completely misleading. The fund manager might actually be net short uranium through other instruments or positions, and the long equity exposure is simply used as a hedge, a relative value trade, or part of a more complex pair strategy.

Without understanding the full portfolio construction, what is held privately, what is hedged, and what exposures are being offset, it’s easy to draw the wrong conclusions from a 13F filing.

Anyway, a glimpse into these portfolios can sometimes provide interesting ideas to research further, whether it’s identifying emerging trends, understanding where smart capital is flowing, or simply learning how different investment strategies are evolving over time.

Unfortunately, this time most of the major fund managers remain heavily long tech, which is not particularly surprising, given that it continues to be one of the few consistently performing areas of the market, alongside the somewhat less glamorous but still “loved by me” chemicals and offshore sectors.

As a result, I haven’t come across many new or differentiated ideas worth digging into from this round of filings. That said, I do have a couple of names on my radar that I’m currently researching and will write about shortly. One of them I actually mentioned in last week’s portfolio update.

I can also share that my cash position has increased. This is not a market to approach lightly: breadth continues to deteriorate, leadership is narrowing further, and several internal indicators are weakening across the board.

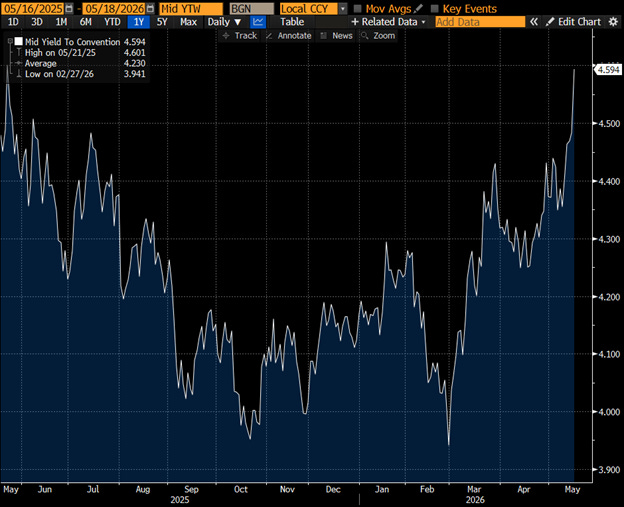

At the same time, the fixed income backdrop is becoming less supportive, with long-end yields pushing higher, most notably the 30-year in Japan reaching new highs, alongside rising rates in both the UK and the US (chart from Bloomberg, 10y yield).

In this kind of environment, caution is always warranted.